The Smooth Forward Price Curve builder for Python

The Smooth Forward Price Curve builder for Python you never thought you needed.

Curvy

This library is based on theory from “Constructing forward price curves in electricity markets” by Fleten and Lemming. The curve is created by solving a constrained optimization problem that ensures that the curve maintains the correct average value for each price period while keeping its smooth and continuous properties.

The library takes a list of forward curve prices and automatically assigns them to a period in the following order: Day Ahead (DA), Balance of Month (BOM), End of Month (EOM) 1, EOM 2, etc… Currently, this is the only format the library supports, but the curve builder is not restricted to this format. If needed, it is very possible to build custom formats and optimize the curve over this.

Installing

Download this package from GitHub. Unzip the file and run python setup.py install.

The simple way

The easiest way to build the forward price curve is to use the build_smfc_curve function. It takes in a list of forward prices and the starting date for trading. For our example, the first value in the forward price list would be the Day Ahead price, so the starting date is actually one day before the first forward price in the list.

Example:

Given a list for forward prices: [3, 4, 6, 5]

Say start_date is 26-11-2018, then the DA date would be 27-11-2018 and the forward price would be 3. BOM would be 28-11-2018 to 30-11-2018 and the forward price would be 4. EOM 1 would be the whole of December with a price of 6 and EOM 2 would then be January 2019 with the price of 5.

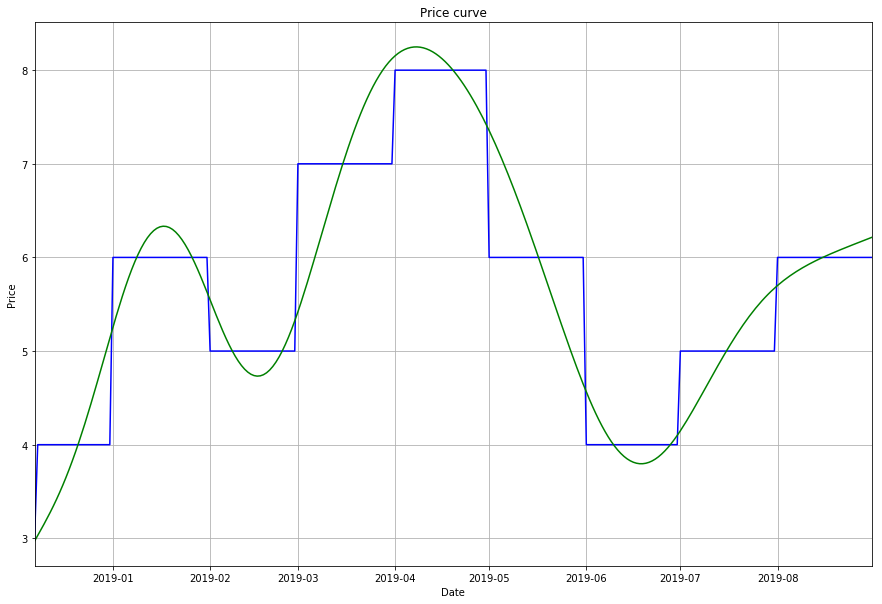

Below we seen an example of how such an expanded curve can be built:

from curvy import builder, plot

import datetime

start_date = datetime.datetime.now()

forward_prices = [3, 4, 6, 5, 7, 8, 6, 4, 5, 6]

x, y, dr, pr, y_smfc = builder.build_smfc_curve(forward_prices, start_date)

fig, ax = plot.mpl_create_curve_plot(x)

plot.mpl_plot_curves(x, y, fig, ax, (x, y_smfc, 'green', '-'))

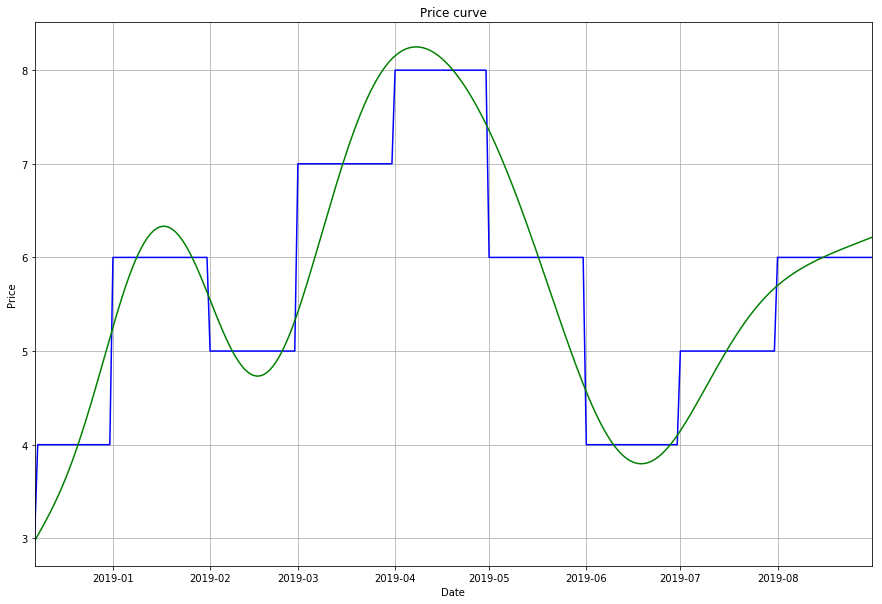

The hard way

The build_smfc_curve function automates most of the process, but limits what we are able to do. Below is an example of how the x-axis date values and indices can be constructed and used to optimized the curve on.

1. Building our x-axis index variables

First we define our initial parameters.

from curvy import axis, plot, builder

import datetime

# Define the starting date we want to contruct the forward curve from

start_date = datetime.datetime.now()

forward_prices = [3, 4, 6, 5, 7, 8, 6, 4, 5, 6]

More info about these functions can be found in the code or by running help(axis.write_some_function_here) in Python.

# First we need the dates representing our x-axis

dr = axis.date_ranges(start_date, 8)

x = axis.flatten_ranges(dr)

The forward prices are expanded to match the date indicies.

# We get the unsmooth forward price for each step

pr = axis.price_ranges(dr, forward_prices)

y = axis.flatten_ranges(pr)

Building the curve parameters

After the index is built, the optimization problem can be solved. This will give us the necessary parameters to calculate the smooth forward curve.

taus = axis.start_end_absolute_index(dr, overlap=1)

knots = axis.knot_index(taus)

H = builder.calc_big_H(taus)

A = builder.calc_big_A(knots, taus)

B = builder.calc_B(forward_prices, taus)

X = builder.solve_lineq(H, A, B)

y_smfc = builder.curve_values(dr, X, builder.smfc, flatten=True)

fig, ax = plot.mpl_create_curve_plot(x)

plot.mpl_plot_curves(x, y, fig, ax, (x, y_smfc, 'green', '-'))

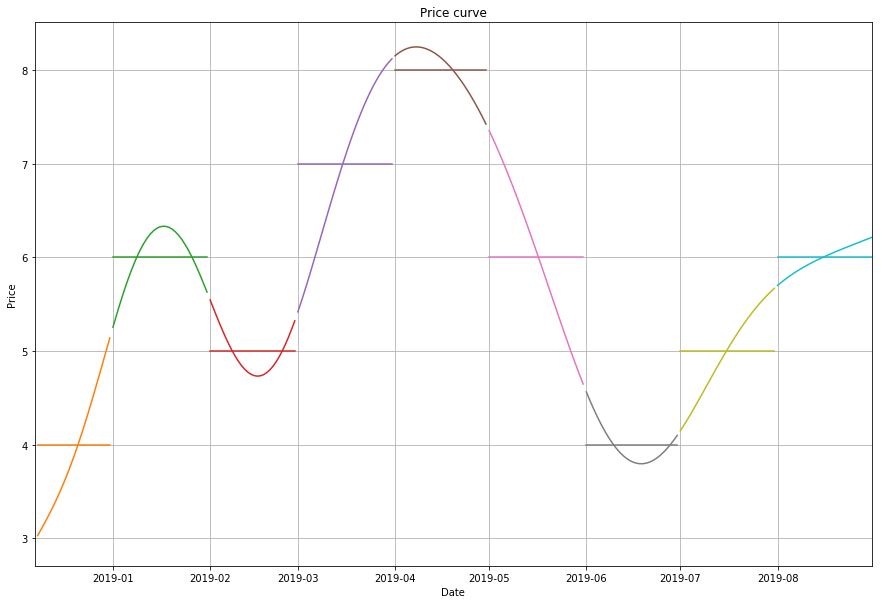

Showing only the segments

y_sfmc = builder.curve_values(dr, X, builder.smfc)

fig, ax = plot.mpl_create_curve_plot(x)

plot.mpl_plot_curve_sections(x, y, fig, ax, (dr, y_smfc), (dr, pr), hide_price=True)

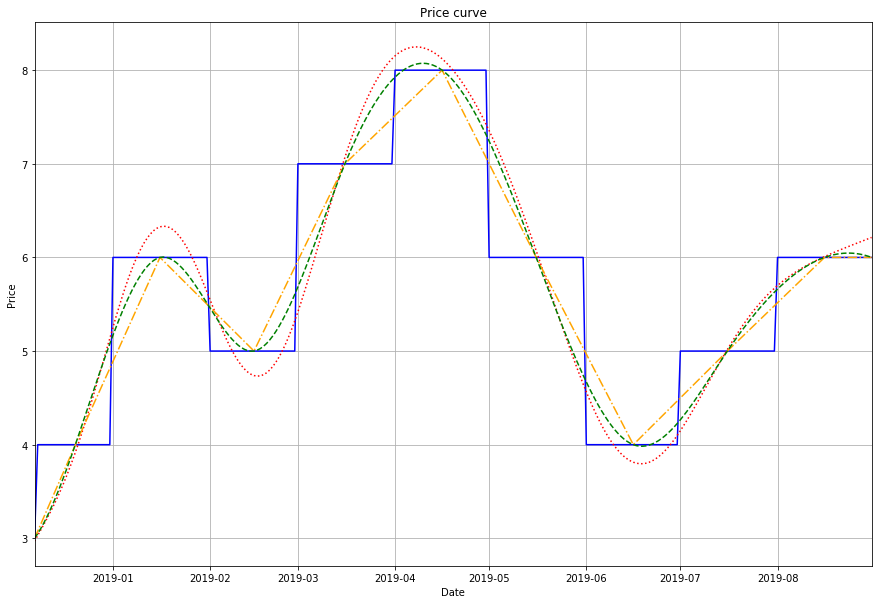

Or customize your own plots

from scipy.interpolate import interp1d

import numpy as np

start_date = datetime.datetime.now()

forward_prices = [3, 4, 6, 5, 7, 8, 6, 4, 5, 6]

fig, ax = plot.mpl_create_curve_plot(x)

x, y, dr, pr, y_smfc = builder.build_smfc_curve(forward_prices, start_date)

pr_mv = axis.midpoint_values(pr, include_last=True)

dr_mai = axis.midpoint_absolute_index(dr, include_last=True)

f_simple = interp1d(dr_mai, pr_mv)

f_cubic = interp1d(dr_mai, pr_mv, kind='cubic')

# We need to convert the indices from dates to numbers

x_i = np.arange(0, len(x))

plot.mpl_plot_curves(

x, y, fig, ax,

(x, y_smfc, 'red', ':'),

(x, f_simple(x_i), 'orange', '-.'),

(x, f_cubic(x_i), 'green', '--'),

)

Correcting the average of the smoothed curve

In areas of rapid change in the forward price, the optimization algorithm struggles to maintain a correct average. If it is important for you to have a very precise average value for each time product, there is a method to correct for that. The correction algorithm works by first creating the smooth curve using the input forward prices. It then removes the difference between the average of the curve and the correct average from the forward prices. From this, a new range of corrected forward prices are created and the curve builder is run one more time based on these values. The average correction can be run by adding corr_avg=True as an input variable to the curve building function:

x, y, dr, pr, y_smfc_corrected = builder.build_smfc_curve(forward_prices, start_date, corr_avg=True)

The end result can be seen in plot below.